Every month, thousands of school accountants across India do the same thing: open a spreadsheet, pull attendance registers, manually calculate PF, ESI, PT & TDS across 80 or 200 or 600 staff records. And then hope they get it right.

Some months they do. Many months they don't. And when the errors surface; in a staff member's salary slip, in a statutory filing, in an audit, the correction cycle that follows costs the institution far more than the time saved by using a spreadsheet in the first place.

Automating payroll for schools and colleges in India is not a luxury reserved for large institutions with dedicated finance teams. It is a systems decision that any school processing more than 20 staff salaries per month cannot afford to keep postponing.

This guide explains why, shows what the manual payroll problem actually costs, and walks through exactly how edumerge HRMS replaces the entire error-prone process with a single, accurate, compliant payroll run.

The Manual Payroll Problem in Indian Schools

In the last week of the month, the accountant pulls attendance data from three separate registers. One for teaching staff, one for non-teaching, one for support staff. And begins reconciling it against the master salary sheet.

- Three staff members applied for leave mid-month; one approval is missing.

- A teacher joined on the 11th of the month and needs a pro-rated calculation.

- Two staff members have advance repayments due, tracked in a separate notebook.

- One staff member moved up a pay grade this month following an increment revision.

Each of these variables requires a manual adjustment to the spreadsheet. Each adjustment is an opportunity for error.

And when the payroll finally runs; often 2-4 days late because of this process, there is no audit trail for any individual calculation.

If a staff member disputes their salary, the accountant has to reconstruct the logic from memory or from handwritten notes.

This is not an edge case. This is how HR payroll management for schools and colleges operates at the overwhelming majority of private educational institutions in India.

And it is a process that generates compliance risk, staff dissatisfaction & administrative overload every single month. Without exception.

The good news: it is entirely solvable.

The transition from manual salaries to smart systems is well-documented, proven, and with the right platform; achievable without disrupting a single pay cycle.

Explore edumerge HRMS.

Quick-Reference: Manual Process vs edumerge HRMS

| Payroll Task | Manual Process | edumerge HRMS |

|---|---|---|

| Attendance data collection | Manual registers, end-of-month reconciliation | Real-time biometric integration, automatic |

| Pay component calculation | Spreadsheet formulas, manual updates | System-configured, automatically applied |

| PF calculation | Manual, formula-based, error-prone | Automated from correct statutory base |

| ESI eligibility and contribution | Manually reviewed each cycle | System-checked against current gross wages |

| PT deduction | Manual, often outdated slab rates | State-specific slabs, auto-applied |

| TDS projection | Annual, rarely updated mid-year | Per-employee projection, updated each cycle |

| Staff advance deductions | Separate notebook / ledger | Integrated, auto-deducted per schedule |

| Salary slip generation | Manual preparation and distribution | Auto-generated and digitally delivered |

| Statutory challans | Prepared manually post-payroll | Generated alongside each payroll run |

| Audit trail | Spreadsheet version history (if saved) | Full, timestamped, permanently retrievable |

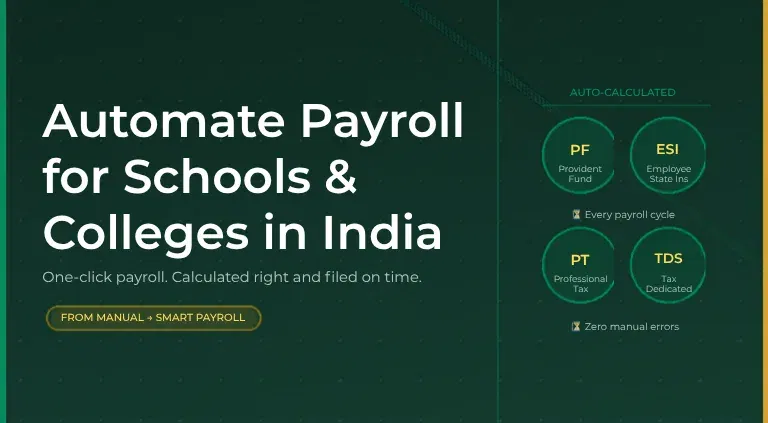

Where the Errors Actually Come From: PF, ESI, PT, and TDS

Manual payroll errors in Indian schools are not random. They concentrate predictably in four statutory areas. And each one of them carries its own compliance consequence.

1. Provident Fund (PF)

Under the Employees' Provident Funds and Miscellaneous Provisions Act, both employer & employee contribute 12% of the employee's basic wages (plus DA & retaining allowance, if applicable) to the EPF.

The critical error in manual payroll: calculating PF on the gross salary rather than the correct statutory base. Or worse, applying the calculation inconsistently across staff categories.

Schools that cap PF contribution at ₹1,800 (the statutory ceiling on the ₹15,000 wage ceiling) for all staff regardless of actual basic wage often do so because someone once configured the spreadsheet that way, and no one has reviewed it since.

The result is years of under-deduction or over-deduction. A liability that compounds silently.

2. Employee State Insurance (ESI)

ESI applies to employees earning up to ₹21,000 per month (gross), with the employee contributing 0.75% and the employer contributing 3.25% of gross wages.

Schools that fail to track gross wage movements; particularly for staff who cross the threshold mid-year after an increment, end up with ESI eligibility errors that are difficult & expensive to correct retroactively.

Contractual or part-time staff at schools are a particular ESI risk area. Whether they are eligible and at what contribution rate requires a specific review; which manual processes rarely prompt.

3. Professional Tax (PT)

Professional tax is a state-level levy. Its rates, slabs & applicability vary by state, and in some states differ by gender.

A school operating across two states, or one that has simply never updated its PT slab after a state revision, is deducting the wrong amount from staff salaries every month. The deduction appears on the salary slip as accurate. It is not.

4. Tax Deducted at Source (TDS) on Salaries

TDS on salary income (under Section 192 of the Income Tax Act) requires monthly tax liability projection for each employee, accounting for declared investments under Chapter VI-A, HRA exemption, standard deduction, and the tax regime chosen by the employee.

In a manual payroll environment, this projection is typically done once at the start of the year and not updated when staff circumstances change. Leading to either systematic under-deduction (liability for the employee at filing time) or over-deduction (cash flow impact for the staff member across the year).

Year-end TDS reconciliation in schools that have managed this manually is routinely painful.

- Form 16 preparation becomes a multi-week exercise.

- Staff receive their Form 16 late.

- And any errors discovered at that point require revised TDS returns, attracting late-filing interest.

You might also like reading about Staff Management Challenges in Educational Institutions.

The Real Cost of Payroll Errors

The direct costs of payroll errors are well-understood: late filing penalties, interest on delayed deposits & correction costs. But the full cost of manual payroll errors in educational institutions extends much further.

Staff trust and retention. A salary slip error, even a small one, signals to a teacher that the institution does not have its systems under control. A correction that takes two weeks erodes trust further. Over time, this payroll inconsistency is a meaningful driver of staff attrition. The relationship between payroll reliability and teacher retention is explored in depth in our piece on how payroll delays drive teacher attrition.

Administrative time cost. A school accountant spending 10–15 hrs/month on manual payroll processing is a cost that automated payroll eliminates almost entirely. Including data gathering, calculation, verification, correction, and salary slip distribution. In a 500-staff institution, this time cost is more evident against whoever assists in the process.

Audit exposure. Schools face PF, ESI, and IT scrutiny at various points in their operating life. A manual payroll history with inconsistent statutory calculations, missing remittance challans, and undocumented adjustments is an audit risk that a well-configured automated system eliminates by design.

Statutory interest and penalties. Late or incorrect PF and ESI remittances attract interest at 12% per annum under the EPF Act, plus damages up to 25% of the arrear amount for delays beyond specified periods. These are recoverable from the institution, not from the accountant who made the calculation error.

What Payroll Automation Actually Means

Payroll automation is not just digitising the spreadsheet.

Moving from a paper register to an Excel sheet is digitisation. It does not eliminate the manual calculation steps, the statutory error risk, or the reconciliation burden. Many believe they have "automated" payroll when they have simply moved their manual process onto a screen.

True payroll automation, delivered through a purpose-built HR and payroll software for educational institutions means:

- Attendance and leave data flow automatically into payroll without manual data entry

- Pay components are calculated by the system based on configured rules, not by a person entering formulas

- Statutory deductions (PF, ESI, PT, TDS) are calculated accurately from the correct base amounts, using the correct rates, automatically updated when regulations change

- Payroll runs are processed in minutes, not days

- Salary slips are generated individually for every staff member and distributed digitally, no manual slip preparation

- Statutory challans and reports are generated alongside payroll, not as a separate manual exercise afterwards

- Every payroll run is fully auditable: every calculation has a documented basis

This is what automating payroll and expense tracking with a School/College ERP platform makes possible. And it is what edumerge HRMS delivers, built specifically for the complexity of educational institution payroll, not adapted from a corporate HR tool.

Read more about: Managing Teacher Attendance | edumerge Leave Management

One-Click Payroll: A Step-by-Step Walkthrough with edumerge HRMS

Here's how a complete monthly payroll cycle runs inside edumerge HRMS. From attendance capture to salary slip delivery, for an Indian school or college processing staff payroll.

Step 1 - Attendance Data Automatically Captured

Staff mark attendance through app or biometric integrated directly with edumerge HRMS. Time-stamped check-in & check-out records in real time. No manual register, no data entry, and no end-of-month reconciliation between attendance and payroll.

Leave applications and approvals processed through the platform's digital leave management workflow with already updated attendance records. Pro-rated calculations for mid-month joiners and exits are handled automatically by the system based on configured joining and separation dates.

Step 2 - Pay Components Applied by System

Each staff member's pay structure; basic, HRA, DA, transport allowance, special allowances, deductions, is configured once in edumerge HRMS at onboarding (or during migration from the previous system).

When payroll runs, the system applies each component according to that configured structure. Increment revisions, grade changes, and pay structure updates are made once in the staff record and auto-reflected in the next payroll cycle.

There is no formula replication across rows, no risk of a copied cell carrying the wrong logic, and no "please check this staff member's calculation" note on a sticky note.

Step 3 - Statutory Deductions Automatically Calculated

edumerge HRMS calculates PF, ESI, PT, and TDS automatically as part of each payroll run. From the correct statutory base amounts, using the correct rates, and reflecting any eligibility changes since the last cycle.

- PF is calculated on the correct basic wage component, with employer and employee shares computed separately.

- ESI eligibility is checked against current gross wage, with contribution rates applied correctly for eligible staff.

- PT is calculated using the correct state slab, updated when state governments revise rates.

- TDS is projected and deducted based on each staff member's annual liability, accounting for declared exemptions and the chosen tax regime.

No spreadsheet formula. No manual cross-referencing of statutory notifications. No annual surprise at year-end when the projections don't match the actuals.

Step 4 - Reconciled Staff Advances and Deductions

Staff advance balances and scheduled repayments maintained within edumerge HRMS are auto-applied in the payroll run. The system deducts the correct instalment from the relevant staff member's net pay, updates the advance ledger, and records the transaction. Without any manual ledger entry or interference required.

Step 5 - Payroll Reviewed and Approved

Before finalisation, edumerge HRMS surfaces a payroll summary for review. Total gross pay, total deductions, total net pay, and individual staff breakdowns, all visible in a single pre-approval screen.

Any anomalies (a significant variance from last month, a missing attendance record, a pending approval) are flagged for review before the payroll is locked.

This review step replaces the hours of cross-checking that manual payroll requires, and the errors that cross-checking still misses.

Step 6 - Salary Slips Automatically Generated and Distributed

Once payroll is approved, edumerge HRMS generates personalised salary slips for every staff member. Itemising every pay component, every deduction, every statutory contribution & net pay, and delivers them digitally. Staff receive their slip the same day payroll is processed.

No printing, no distribution, no "can you resend my slip" requests.

Step 7 - Statutory Challans and Reports Generated

Alongside salary slip generation, edumerge HRMS produces the statutory reports and challans required for PF remittance, ESI remittance, and PT filing. Formatted for the relevant regulatory submission.

TDS workings are maintained in the system throughout the year, making Form 16 preparation at year-end a system-generated output rather than a multi-week manual exercise.

And the best part? All this happens with a full audit trail. Every payroll run, every calculation, every approval is permanently documented and retrievable. Supporting internal review and external audit equally.

The Case for Acting This Year

The transition from manual payroll to an automated system is not a multi-year technology project. With edumerge HRMS, institutions migrate their staff data, configure pay structures, and are processing their first automated payroll cycle within weeks.

The cost of waiting, in monthly error-correction time, compliance exposure, staff trust erosion & audit risk, is measurable and ongoing.

Every manual payroll cycle that runs is an opportunity cost relative to what an automated system delivers.

To see how edumerge HRMS handles payroll for your institution's specific staff structure, visit the edumerge HRMS product page.

Or speak with the team about a walkthrough built around your payroll complexity.

Frequently Asked Questions (FAQs)

1. What is the best payroll software for schools and colleges in India?

The best HR and payroll software for educational institutions in India is one built specifically for the complexity of the education sector, not adapted from a corporate HR tool. edumerge HRMS is purpose-built for this use case, serving schools and colleges across India.

2. What statutory deductions must the Indian school payroll process each month?

Indian school payroll must correctly process Provident Fund (PF), Employee State Insurance (ESI), Professional Tax (PT), and Tax Deducted at Source (TDS) on salary.

3. How does automating payroll reduce errors in schools?

Payroll automation eliminates the three most common error sources in manual school payroll:

- Incorrect data inputs (resolved by feeding attendance and leave data directly from integrated systems),

- Incorrect calculation logic (resolved by replacing manual formulas with a system-configured calculation engine), and

- Outdated statutory rates (resolved by maintaining current PF, ESI, PT, and TDS rules within the platform).

4. Can edumerge HRMS handle payroll for both teaching and non-teaching staff?

Yes. edumerge HRMS processes payroll across all staff categories simultaneously. From teaching staff, non-teaching administrative staff, to support staff, contractual faculty, visiting faculty, and any other category with its own configured pay structure.

5. How long does payroll take with edumerge HRMS compared to manual processing?

Manual payroll at a 100-staff school typically takes 8–15 hours/month when all steps are included. Including data collection, calculation, verification, correction, slip preparation, and distribution. With edumerge HRMS, once configuration is complete, a full payroll cycle; from attendance data pull to salary slip delivery, can be completed in under a few hours.